Health Insurance: Government mandate? Does it even work?

Many people think that their insurance company has their best interest and health as a top priority. Unfortunately, nothing could not be farther from the truth. The health insurance companies have one goal in mind: maximizing revenue and profits at any cost. They want you as sick as possible for as long as possible to increase utilization of the system. Health insurance companies make the most money off their sickest patients.

Is mandated health insurance a good choice for patients?

After the Affordable Care Act was passed, Americans received a mandate to purchase health insurance from the same companies who provide health insurance to employers. Who was the largest lobbying group supporting the Affordable Care Act? Health insurance lobbyist! Another government mandate that only seems to benefit large corporate interests who generally provide subpar coverage, are expensive and provided by the same companies that promote a volume/profit-based health care environment.

Increases in costs occur every year including premiums, maximum annual out of pocket expenses and deductibles all while services dwindle with the insurance carrier dictating which doctors, hospitals, and pharmacies you can visit, what laboratories are approved, what procedures or tests are appropriate and what medications will be allowed. Your insurance company dictates when, where, who and how your healthcare is provided by choosing which services to cover and which services are not covered. Are the decision makers at insurance companies trained medical professionals? Health insurance companies are playing doctor and practicing medicine without a license! A felony.

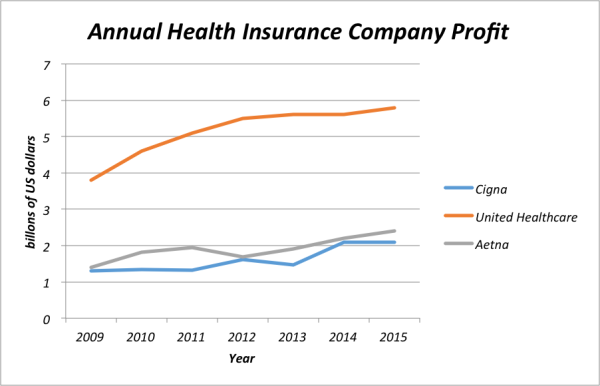

Real costs of employer provided health insurance coverage

The Kaiser Family Foundation released a report in 2015 which found that Americans with employer sponsored health insurance plans paid an average of $4,955 per year in premiums. In addition, the employer paid another $17,545 per year totaling $22,500 per year for an individual health insurance plan before the insured individual met their annual deductible.

Where does all that money go? It goes to record profits for health insurance companies with bloated administrative and executive compensation. For example, in 2022 the CEO of Molina, an insurance company that receives all its revenue from government funded programs, was paid $181 million dollars in salary. The insurance company takes in your premiums and when you don’t need medical care or they deny paying for it, the money you pay goes straight to profit the company, its executives, and its stockholders.

Real cost of individual health insurance plans

A good individual health insurance plan costs the insured an average of $6,800 per year in medical expenses before the insurance carrier begins to pay. When the insurance does pay it is typically 80% of the cost; this leaves the insured customer on the hook for the remainder. Higher deductible plans will come with lower premiums and lower reimbursement rates, leaving the insured customer paying for most of their health care costs out of pocket. The most vulnerable patients are the uninsured as they have no bargaining power over the cost of their health care and are often left paying inflated health care costs which can be 10-15 times higher than the actual cost. This is a common practice which helps medical facilities show big losses which amount to large tax write-offs at the end of the year. This is how health insurance companies make record profits.

Why is it bad for doctors? Why are doctor’s opting out of taking insurance?

The typical doctor’s office will collect a copay (also rising every year) and bill the insurance company for the remainder of the patient visit, often in the $600-$800 range for a new patient visit. One physician may need to hire several staff for coding, billing, filling out prior authorizations in addition to a front desk person, a medical assistant, and an office manager. In addition, a physician may wait as long as 24 months to get reimbursement from the insurance company that usually reimburses at only a fraction of the original amount billed. The doctor’s office must then seek the remainder from the patient, adjust the invoice down, or continue the losing battle with the insurance company. Under this model, to make ends meet, most primary care physicians must see 7-8 patients an hour, leaving approximately 7 minutes of face-to-face time with your provider.

In a free market where competition helps to keep costs down, costs will usually decline over time. In the health insurance market, there is no transparency and every year health care costs are going up. This lack of fairness and transparency allows health insurance companies to increase their revenue and profits every year without any accountability, paving the way for them to set record profits meanwhile leaving patients and providers on the hook for the increased cost. We are the only developed country that regularly bankrupts citizens for inflated and uncollected health care fees.

What do we do?

Here at Thrive Medical LLC we are starting a health care rebellion. We have opted out of the system in that we do not accept insurance for patient visits so that we can provide superior, transparent, fair, and equitable care for each patient (we do run everything else through insurance). We encourage others to do the same and go to a direct pay system that is transparent, benefits the patient and doctor by eliminating the middleman and greatly increases patient satisfaction. Our direct pay model provides price transparency, charges average half of what most doctors charge and our model allows the doctor to provide the highest level of care spending all the time necessary to treat and cure the patient.

Don’t miss our March 2023 Thrive Newsletter and be sure to follow us for news and fun at Facebook.

{kind=link}

{kind=link}

{kind=link}

{kind=link}